How to improve your SCHUFA Score in Germany #

In this guide, you’ll learn what a strong financial history in Germany means, how your SCHUFA score affects insurance and contracts, and the best ways to improve your SCHUFA score.

What is a strong financial history in Germany? #

A strong financial history in Germany usually means:

- You have a stable, regular income

- You pay your bills on time

- You have a positive credit history

Your credit history is mainly measured by your SCHUFA score.

This score is checked for many everyday applications, including:

- Mobile phone contracts

- Internet and electricity providers

- Apartment rentals

- Bank accounts & loans

- Private health insurance

If your SCHUFA score is low, you may be rejected or asked to pay deposits and higher fees.

What is SCHUFA? #

SCHUFA stands for Schutzgemeinschaft für allgemeine Kreditsicherung, which means Protection Association for General Credit Security. It is a private organization in Germany that collects financial data from banks and service providers to calculate your credit risk. This helps companies decide whether or not to enter into a financial agreement with you.

A bad SCHUFA score can prevent you from:

- Renting an apartment

- Signing a phone contract

- Getting a loan

- Obtaining private health insurance

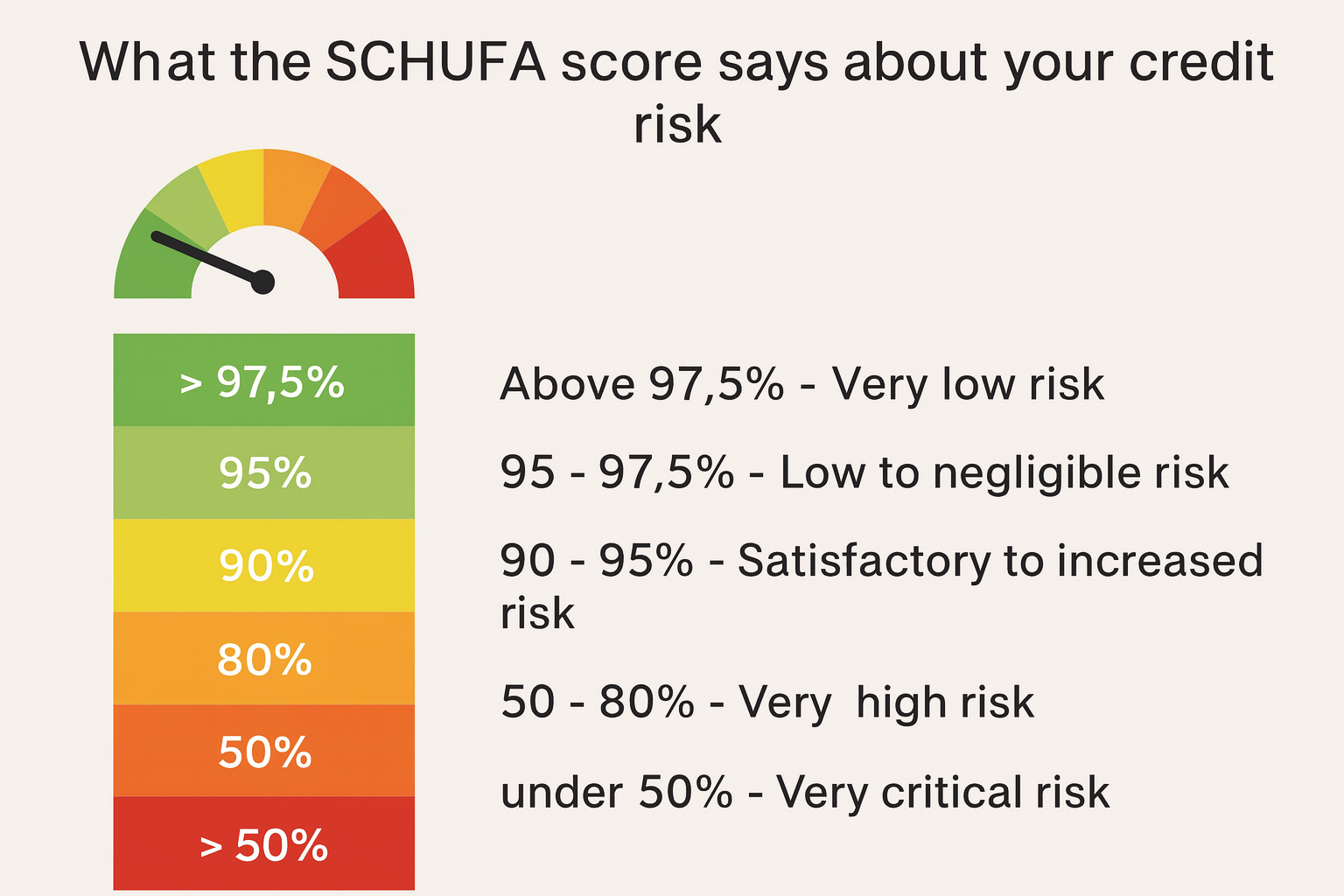

How to read your SCHUFA score #

Your SCHUFA score is shown as a percentage between 0% and 100%.

In most situations, a score above 95% is good enough for contracts, banking, and insurance. Every person in Germany is entitled to one free SCHUFA report per year.

If you find incorrect information in your report, you have the right to request a correction or deletion.

When is SCHUFA data deleted? #

- Paid debts under €2,000 are deleted after 3 years (if paid within 6 weeks)

- Negative entries of minors are deleted once the debt is paid

- Old data is automatically removed after the legal retention period

What information does SCHUFA collect? #

SCHUFA may collect and store data such as:

- Your personal details (ID, address, Anmeldung)

- Bank accounts and credit cards

- Active loans or financing

- Phone and internet contracts

- Leasing agreements

- Installment purchases

- Guarantees (Bürgschaften)

- Late or missed payments

It does not store:

- Your salary

- Your profession

- Your nationality or religion

How to improve your SCHUFA score #

Here are the most effective ways to improve your SCHUFA rating in 2025:

1. Request your SCHUFA report #

Always start by checking your report. Look for:

- Incorrect addresses

- Unknown contracts

- Wrong payment records

You can challenge and remove false information. There are lawyers who specialize in SCHUFA corrections. To save costs, legal insurance (Rechtsschutzversicherung) can be helpful.

2. Pay off open Debts #

In Germany, paying your debt is positive. Once the status changes to “settled,” the entry will be deleted after a maximum of three years.

3. Close unused Bank & Credit Accounts #

Too many open accounts can lower your score. Close:

- Old checking accounts

- Unused credit cards

- Forgotten online payment methods

4. Keep your address stable #

Moving often can lower your score. If possible, avoid frequent relocations.

5. Always Pay on Time #

Even a small missed payment (e.g. €60 for public transport fine) can drop your score significantly.

Set up:

- Automatic payments (SEPA Lastschrift)

- Reminders for important bills

Conclusion

Improving your SCHUFA score in Germany doesn’t have to be complicated. If you regularly pay your bills on time, keep an eye on your SCHUFA report, clear open debts, and avoid too many unused accounts or frequent address changes, your score will usually improve over time.

A strong SCHUFA score gives you more freedom: better chances for apartments, contracts, loans, and private health insurance. Start with small steps today, and your future self will thank you.

Leave your comment